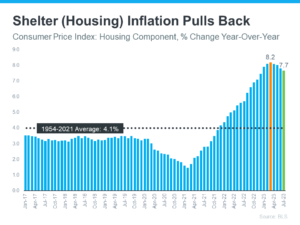

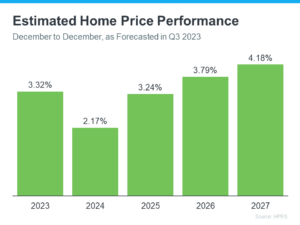

Looking Ahead: Home Price Projections If you’re in the market for a new Raleigh home, one crucial factor to consider is what the experts anticipate for future home prices and how that might influence your investment. While you may have encountered negative news about home prices over the past year, the reality is far more […]