Key Takeaways:

- Buying a home is more affordable today compared to the historical average, partially due to unprecedented low mortgage rates.

- Waiting to purchase a home could cost you money in the long run, especially if your rent payments are impacted by inflation.

- Linda Craft & Team wants you to know that you can afford homeownership—contact our team of top Triangle Realtors today to discuss your financing options.

Yes, Buying a Home Is Still Affordable

The last year of primarily staying at home has reinforced the importance of one’s living space. Because of this, renters are making the leap into homeownership, while some homeowners are considering moving to new homes that better fit their current lifestyles. As home prices continue to appreciate in today’s red-hot real estate market, you may be wondering how affordable it is to buy a home right now. Well, you’re in luck—the real estate experts at Linda Craft & Team are here to address the concerns you have about the affordability of homeownership.

Homes are more affordable today than the historical average

The National Association of Realtors (NAR) produces a Housing Affordability Index to determine an overall affordability score for housing based on three factors—mortgage rates, mortgage payments as a percentage of income, and home prices. In simpler terms, the index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a median-priced home. According to NAR’s methodology, “…a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.”

In the above graph dating back to 1990, the blue bar represents today’s housing affordability. Considering that the higher the index, the more affordable it is to purchase a home, we can see that homes are more affordable now than they’ve been since the housing crash. Properties were sold at never-before-seen discounts during the housing crash, which explains that time period’s unusually high housing affordability.

Why are homes so affordable today?

This year’s homes clearly aren’t being sold at huge discounts like they were during the housing crash, so why are they more affordable today than at any time in the last eight years? Well, that can be attributed to historically low mortgage rates. Buying a home while mortgage rates are unbelievably low may save you money over the life of your home loan.

Is homeownership more affordable than renting?

Now that you know buying a home is actually affordable, you may be wondering how the cost of homeownership compares to renting. Mike Loftin, author of Homeownership Is Affordable Housing, points out that renters pay a higher percentage of their incomes toward rental payments than homeowners pay toward their mortgages. In fact, Loftin’s report cites that “…the typical homeowner household spends 16 percent of its income on housing, while the typical renter household spends 26 percent.”

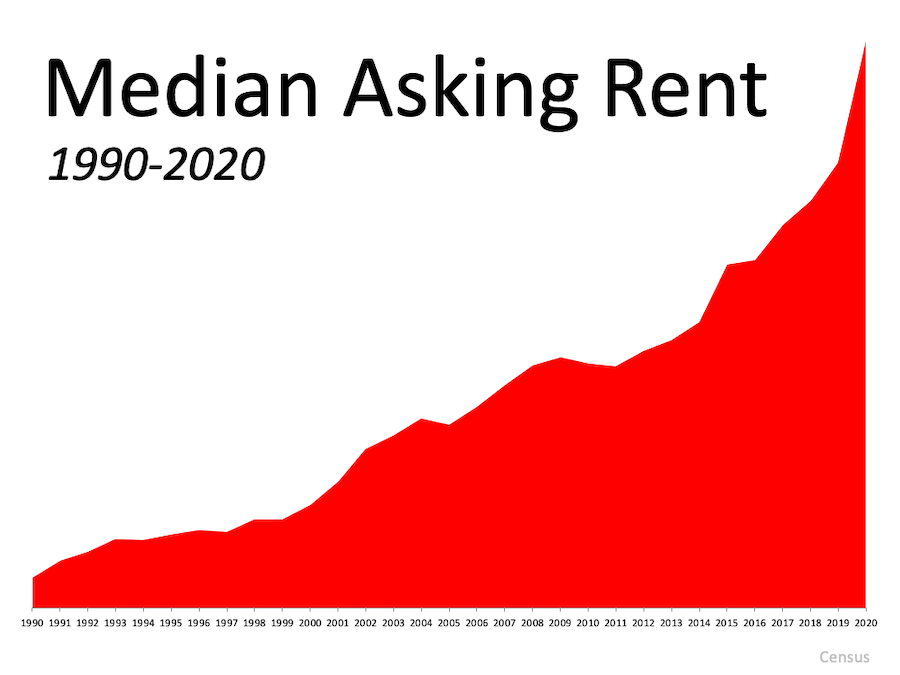

Your mortgage payment remains the same, whereas your rent…

Renters are vulnerable to cost increases unlike homeowners—because nobody rebuys the same house every year. For the majority of homeowners with fixed-rate mortgages, monthly payments can increase only if property taxes and insurance costs go up. The largest portion of a homeowner’s expense—the principal and interest portions of the monthly mortgage—is fixed. On the other hand, a renter’s entire payment is sensitive to inflation. As shown in the above graph, rent payments can increase drastically over time depending on the housing market.

Wanting to Buy a Home? Let Us Help!

Buying a home is one of the largest financial assets you can acquire, and it could save you a significant amount of money over time based on historical affordability trends. Don’t let waiting to buy a home cost you—contact Linda Craft & Team today to discuss your financing options and any other questions you may have. We look forward to walking you through this exciting new chapter!