If you’ve been putting off buying a home in the Triangle area because you thought qualifying would be too difficult, there’s good news: learning how to qualify for a mortgage is becoming a bit easier—without returning to the risky lending practices of the past.

Lenders are loosening up slightly for well-qualified buyers, opening the door to more financing opportunities for those ready to make a move.

So, if strict requirements kept you on the sidelines, this shift could be the opportunity you’ve been waiting for—while still keeping the housing market stable and secure.

Lenders Are Making It Easier To Qualify for a Mortgage

Banks are expanding access to credit to help boost housing activity, including for buyers with lower credit scores or smaller down payments. That means more hopeful Raleigh homeowners are getting approved.

But don’t worry—we’re not heading into another 2008-style crash. Even with this shift, today’s lending standards remain much stricter than they were before the housing crisis.

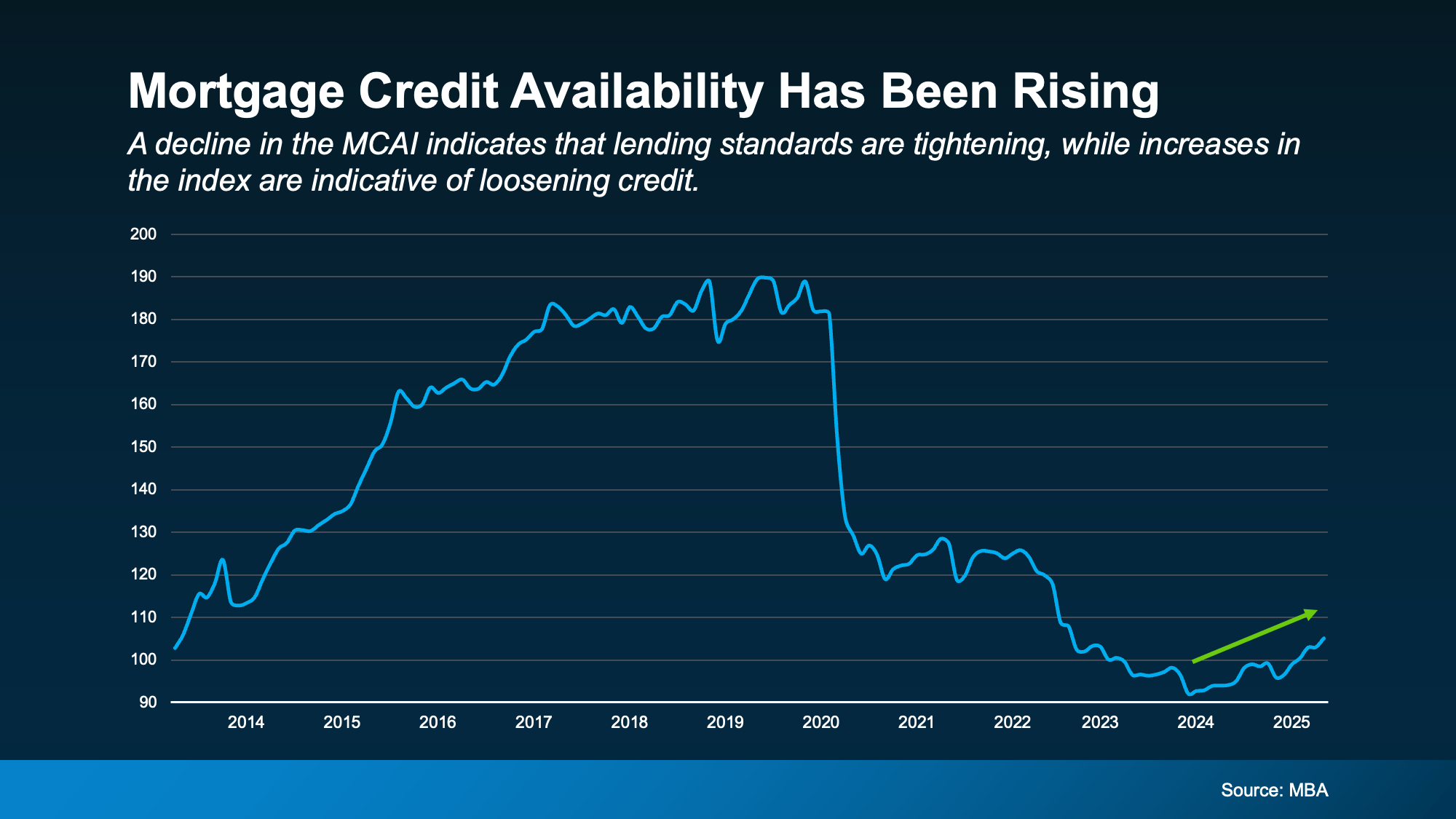

One way to measure this is through the Mortgage Bankers Association’s (MBA) Mortgage Credit Availability Index (MCAI). This index tracks how easy it is for buyers to secure a mortgage.

When the index rises, it signals looser lending. In May, the MCAI reached its highest level in nearly three years (see graph below).

So why does this matter to you? Because it means you may now qualify for a mortgage that would have been out of reach just a few months ago. According to the National Association of Mortgage Underwriters (NAMU):

Mortgage credit availability surged in May, reaching its highest level since August 2022. The uptick signals that lenders are increasingly willing to loosen underwriting standards, providing borrowers with greater access to financing options . . .”

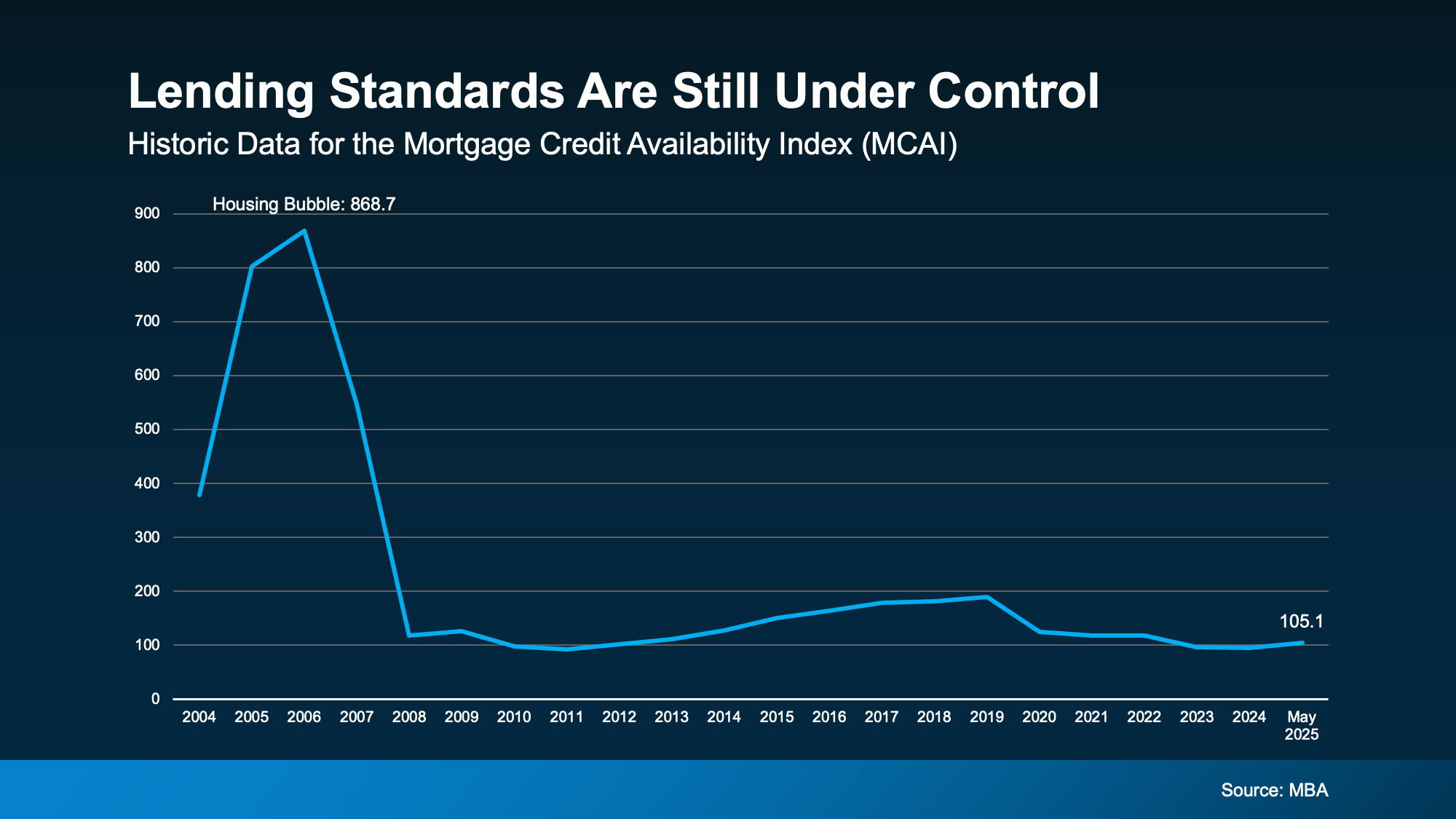

This Isn’t a Repeat of 2008

You might be thinking, “Didn’t looser lending standards cause the 2008 crash?” That’s a fair concern—and it’s smart to ask. But there’s a big difference this time around. Even with more mortgage options available, the guardrails are still in place.

Looking at MCAI data going back to 2004, today’s lending practices remain far more cautious than what we saw during the housing bubble (see graph below).

This shift isn’t a red flag—it’s a positive development for today’s homebuyers. As Brett Hively, SVP of Mortgage, Finance, and Strategy at Ameris Bancorp, recently explained:

This uptick is opening the door for many borrowers to move forward with a home purchase or a refinance program.”

Bottom Line

If you’ve been holding off because you weren’t sure how to qualify for a mortgage, it’s time to revisit your options. Lending standards are still strong—but more accessible than before. Contact Linda Craft Team Realtors to explore whether now is your moment to move toward homeownership in the Triangle area.