According to Fannie Mae, 90% of buyers either overestimate the credit score needed to buy a home or don’t know what lenders are actually looking for.

That means many potential buyers assume their credit score isn’t good enough, and that can create unnecessary fear or delay. But in reality, the credit score to buy a home might be lower than you think. Let’s take a closer look at the facts so you can move forward with confidence.

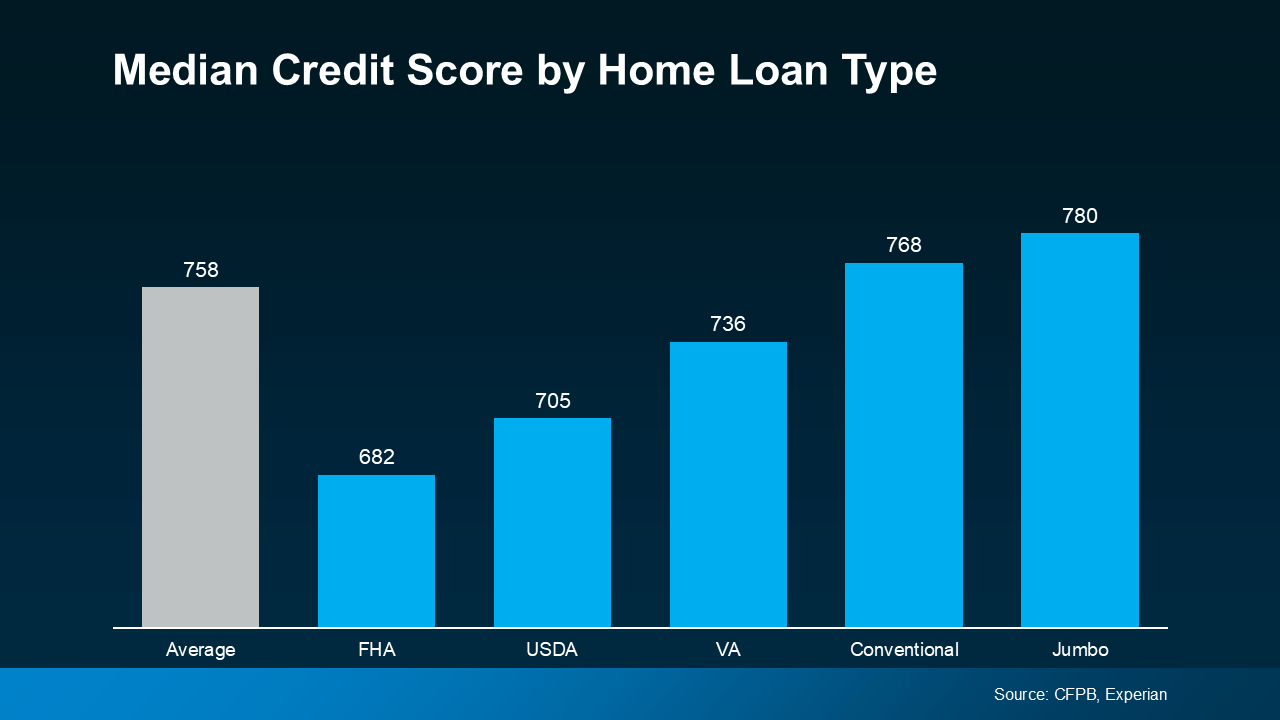

There’s No Single Credit Score You Must Have

There’s no magic number that applies across the board when it comes to the credit score to buy a home. It all depends on the type of loan, the lender’s requirements, and other factors like your income and debt-to-income ratio. Take a look at this breakdown of the median credit scores by loan type, and you’ll see just how much flexibility there is.

While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Credit Score Still Matters

Even though the required credit score to buy a home in the Triangle area varies, it’s still one of the biggest factors lenders consider. A higher score can open doors to better loan terms, lower interest rates, and greater purchasing power. As Bankrate explains:

Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

So even if you’re eligible with a lower score, improving your credit could still save you money long-term.

Want To Boost Your Score? Try These Tips

If you’re hoping to improve your credit score to buy a home, here are a few simple, proven strategies recommended by the Federal Reserve:

- Pay Your Bills on Time: Consistent, on-time payments are one of the biggest factors in your credit score. This includes credit cards, rent, utilities, and even phone bills.

- Pay Down Your Balances: Using too much of your available credit can hurt your score. Keep your credit utilization low by paying down existing debt.

- Review Your Credit Report: Check your credit report for errors and dispute anything incorrect. A clean report can give your score a boost.

- Avoid Opening New Accounts: Opening new credit lines before buying a home can temporarily lower your score. Hold off on new applications while you’re preparing to buy.

Bottom Line

The credit score to buy a home doesn’t have to be perfect. In fact, many Raleigh buyers are eligible for financing even if their score isn’t stellar. But understanding how your score impacts your options—and improving it where you can—can make a big difference.

If you’re unsure where you stand or want to explore your options, contact Linda Craft Team Realtors. We’ll help you navigate the process and determine what steps to take next.