If you are like many Triangle area homeowners, you have probably had this thought: “I want to move, but I do not want to give up my 3% mortgage rate.” That hesitation makes sense. A low rate has likely been one of your biggest financial advantages. Still, there is an important reminder to keep in mind.

A great mortgage rate cannot fix a home that no longer fits your life. As circumstances change, your housing needs can change too. And more Triangle area homeowners are starting to act on that reality.

The Lock-In Effect Is Starting To Ease

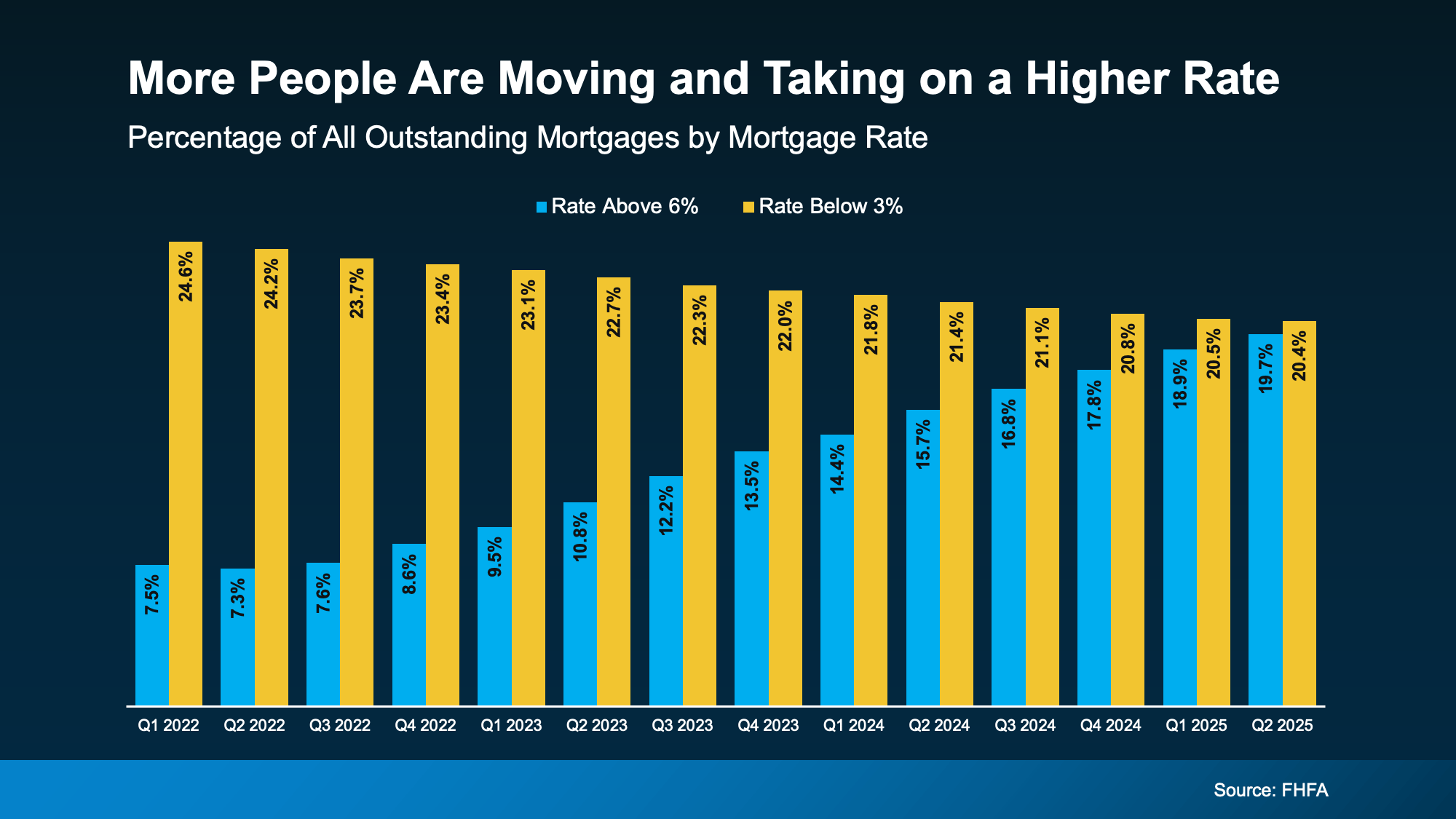

For the past few years, many homeowners have stayed put due to what experts call the lock-in effect. This happens when homeowners avoid moving because they do not want to trade a low mortgage rate for a higher one. However, data from the Federal Housing Finance Agency (FHFA) shows this effect is beginning to loosen.

The share of homeowners with mortgage rates below 3% (shown in yellow on the graph below) has been gradually declining as more people choose to move. At the same time, while some homeowners with rates above 6% are first-time buyers, the portion of homeowners taking on rates over 6% (shown in blue) is growing as repeat buyers make their next move.

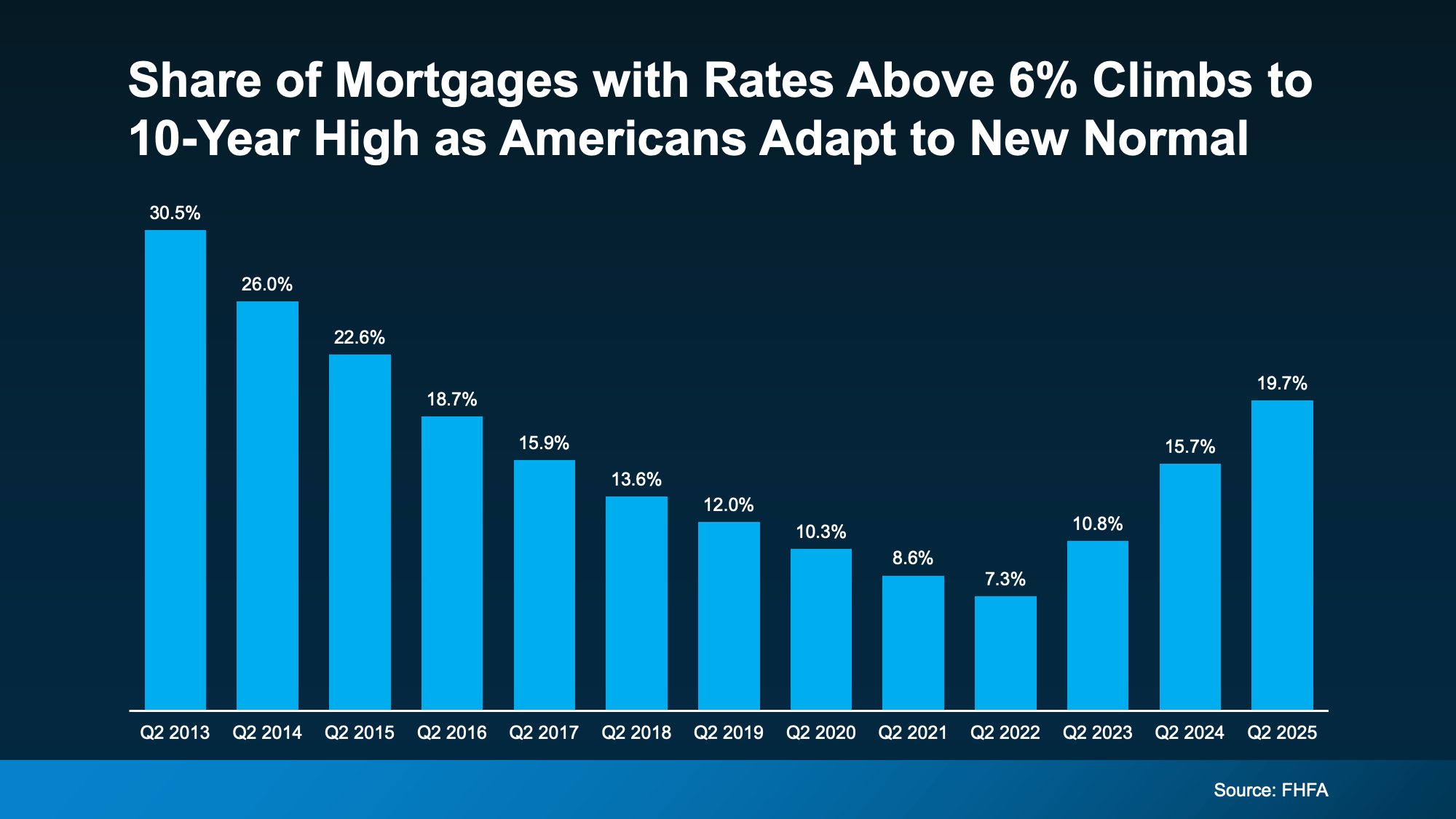

While the shift may seem subtle, it is significant. In fact, the percentage of mortgages with rates above 6% has reached a 10-year high (see graph below). This signals that more homeowners are adjusting to current rates and accepting them as the new normal.

Why Are More People Moving Now, if It Means Taking on a Higher Rate?

The answer is straightforward. Many people can no longer pause their lives. Families expand, careers evolve, priorities change, and a home that once worked well may no longer meet those needs, regardless of how favorable the mortgage rate is. As Chen Zhao, Head of Economic Research at Redfin, explains:

More homeowners are deciding it’s worth moving even if it means giving up a lower mortgage rate. Life doesn’t standstill—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate.”

First American groups these life changes into what they call the 5 Ds:

- Diplomas: People with college degrees typically earn more, and that adds up to more buying power. Maybe you bought your house when you were younger and now that you’ve graduated and have a rising career, you’re ready to move up.

- Diapers: You’ve outgrown your space. If you’re welcoming a new baby, your current home might not be cutting it anymore.

- Divorce: Whether it’s ending a marriage (or starting one),it can create the need for a new place to call home.

- Downsizing: You’re ready to downsize. Maybe the kids have moved out and it’s time to simplify. Smaller house, less maintenance, more freedom.

- Death: If you’ve recently lost a loved one, maybe you’ve realized you want to be closer to family. Life’s too short to live far from the people who matter most.

No matter the reason, there is one key consideration. While a low mortgage rate is valuable, staying in a home that no longer fits may mean putting your life on hold.

According to Realtor.com, nearly two out of three potential sellers have been considering a move for more than a year. That is a long time to delay personal goals, family plans, or lifestyle changes. At that point, the real question may not be whether to move.

It may be how long you are willing to stay somewhere that no longer supports the life you want.

Mortgage rates have already come down from their earlier peak, and forecasts suggest they may ease slightly more in 2026. When you combine that with meaningful life changes, moving may feel more achievable than it did before.

Bottom Line

Life does not wait for the perfect mortgage rate, and you may not need to either.

With rates lower than their recent highs and expected to soften a bit more in 2026, making a move could be more realistic than you think. If you are ready to explore what options make sense in today’s Triangle area market, contact Linda Craft Team Realtors to connect and talk through what comes next.