Understanding the Connection

Have you ever wondered how inflation affects the housing market? The truth is, that these two economic forces are closely intertwined. Changes in one invariably influence the other. Here’s a straightforward overview of the relationship between inflation and the housing market.

The Interplay Between Housing Inflation and Overall Inflation

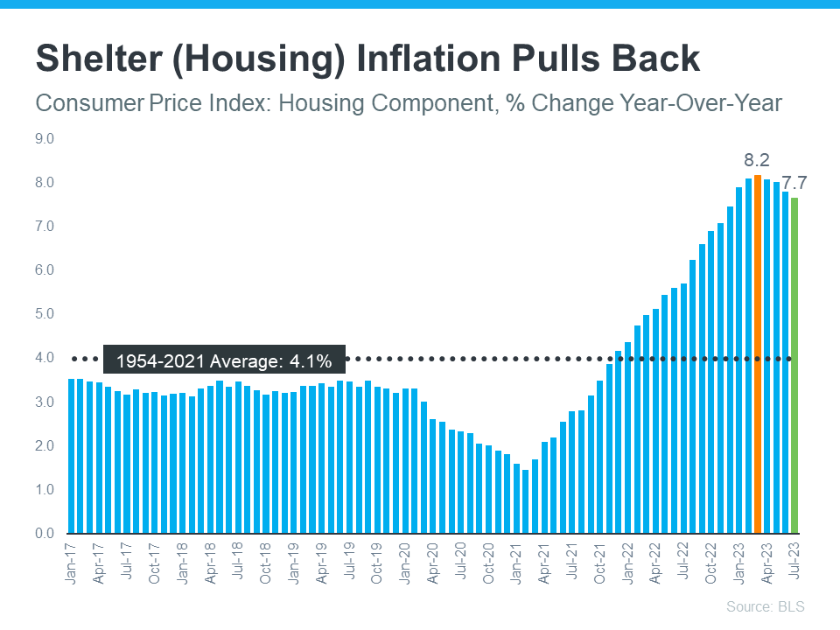

Shelter inflation, as the term implies, measures price growth in the realm of housing. This critical metric is derived from a survey by the Bureau of Labor Statistics (BLS), inquiring both renters and homeowners about their housing costs. Renters divulge their monthly rent expenses, while homeowners disclose the hypothetical rent they’d charge if they were renting out their Triangle area homes.

Shelter inflation mirrors overall inflation in measuring the cost of living but specifically focuses on housing costs. In an interesting twist, shelter inflation has shown a downward trend over the past four consecutive months, as indicated by the survey (see the graph below):

The Significance of Shelter Inflation

Why is this noteworthy? Shelter inflation accounts for roughly one-third of overall inflation, as measured by the Consumer Price Index (CPI). Consequently, fluctuations in shelter inflation inevitably lead to noticeable ripples in overall inflation. This recent decline in shelter inflation might be a precursor to a decrease in overall inflation in the months ahead.

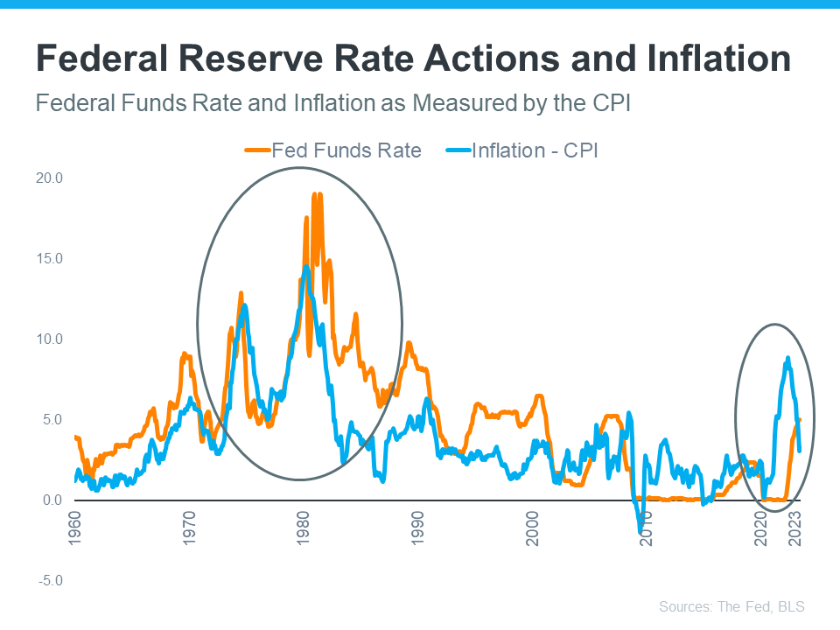

Such a moderation in inflation would be a welcome development for the Federal Reserve (the Fed), which has been diligently working to curb inflation since early 2022. While they have made significant progress (inflation peaked at 8.9% in the middle of last year), they are still striving to achieve their 2% inflation target (the latest report places it at 3.3%).

Inflation and the Federal Funds Rate

How has the Fed been addressing inflation? They’ve been steadily raising the Federal Funds Rate, a key interest rate that influences interbank borrowing costs. When inflation begins to rise, the Fed responds by increasing the Federal Funds Rate, acting as a control mechanism to prevent the economy from overheating.

The circled section of the graph highlights the most recent surge in inflation, the Fed’s actions to raise the Federal Funds Rate to combat it, and the subsequent moderation of inflation in response to these measures. As inflation approaches the Fed’s current 2% goal, it may not require further substantial increases in the Federal Funds Rate.

Potential Implications for Mortgage Rates

So, what does this intricate economic relationship mean for you? While the Federal Reserve’s actions don’t directly determine mortgage rates for your Raleigh home, they do exert an indirect influence. As Mortgage Professional America (MPA) explains:

“. . . mortgage rates and inflation are connected, however indirectly. When inflation rises, mortgage rates rise to keep up with the value of the US dollar. When inflation drops, mortgage rates follow suit.”

While predicting future mortgage rates is challenging, it is encouraging to observe signs of inflation moderation in the economy. This potential decline in inflation’s intensity could bode well for individuals seeking favorable mortgage rates.

Inflation’s Lasting Impact

The connection between inflation and the housing market highlights the intricate web of interconnected economic factors. Every decision, no matter how subtle, can send ripples through different aspects of the economy. As we observe this complex interaction, it’s essential to stay attuned to the nuanced relationship between inflation and the housing market, as it has a more significant impact on our financial decisions than we might realize. Contact Linda Craft Team Realtors for your Triangle area real estate needs.